Is the First Home Guarantee Really Worth It? Rising Rents May Have Just Changed the Game

By Craig Andriessen — Andriessen Property

The federal government’s First Home Guarantee Scheme expanded again recently, giving first-home buyers the chance to get into the market with just a 5% deposit — no Lenders Mortgage Insurance (LMI) required.

On paper, that sounds like a dream. But like everything in real estate… there’s more to the story.

According to new data from research group Cotality, skyrocketing rental prices have changed the way we should view the scheme — and in many cases, getting into the market early may cost less than waiting for the traditional 20% deposit.

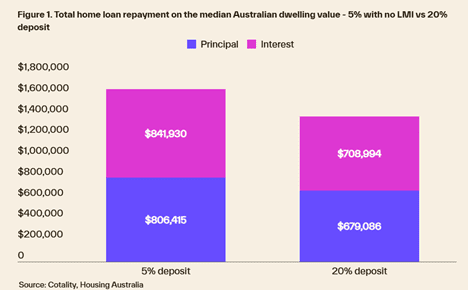

The Catch: A 5% Deposit Also Means a Much Bigger Loan

Let’s be clear — going in with only 5% reduces your upfront pain, but it increases your mortgage debt to 95%.

Cotality crunched the numbers on an average Australian home and found that buyers who take up the scheme could pay tens — even hundreds — of thousands more in interest over a 30-year loan compared to someone who waits and saves a full 20%.

But Here’s the Twist — Renting Is Now So Expensive That Waiting May Cost Even More

Since the scheme was first introduced in 2020, the median Australian rent has jumped by $200 per week. That’s over $10,000 a year going straight to someone else’s mortgage.

While a bigger loan means more interest… waiting years longer to save that 20% might be even more expensive.

In Sydney, Cotality estimates that using the scheme on a $1.5m home could:

- Shave 12 years off the time needed to save a full deposit

- Save roughly $502,000 in rent

[

What’s the Verdict?

Cotality’s Head of Research, Eliza Owen, puts it well:

“Even though a smaller deposit means paying more interest over time, it could still work out cheaper for renters. Getting into a home sooner may mean spending less time paying rent — and those savings can add up.”

My Take as a Local Agent of 30+ Years

From what I’m seeing on the ground in Newcastle and Lake Macquarie, I’d say this:

If you’re renting and struggling to save faster than rents are rising — the scheme might be your chance to jump ahead.

If you’re already living rent-free (with parents, partner or in your own home), it may be worth holding out for a 20% deposit instead.

Either way, don’t make the decision based on theory — run the numbers for your situation.

A Final Word of Caution

This scheme doesn’t fix the real problem — housing affordability. It boosts demand without adding supply, which means more competition at the lower end of the market. In simple terms — more buyers chasing the same homes drives prices up.

So, if you’re thinking of using the scheme… move strategically and move fast.

Want to Talk Strategy?

I’ve helped hundreds of first-home buyers and parents helping their kids into the market — and with government rules changing every five minutes, it pays to have someone who actually reads the fine print (so you don’t have to).

Give me a call on 49548833 for an obligation free chat.